Mirror Wills vs. Single Wills: Which One Do You Need? (2026 Guide)

When you sit down to plan your legacy with a partner, one of the first decisions you’ll face is whether to create Single Wills or Mirror Wills. For many couples in the UK, the choice seems simple: “We want the same things, so let’s just copy each other.”

However, as of 2026, with families becoming more blended and financial lives more complex, the “Mirror” option isn’t always the perfect fit. Choosing between these formats requires more than just checking a box; it demands a clear-eyed look at your family structure, potential future liabilities, and your long-term estate goals. Understanding the subtle legal differences between these two can save your family from significant legal headaches and inheritance disputes in the future.

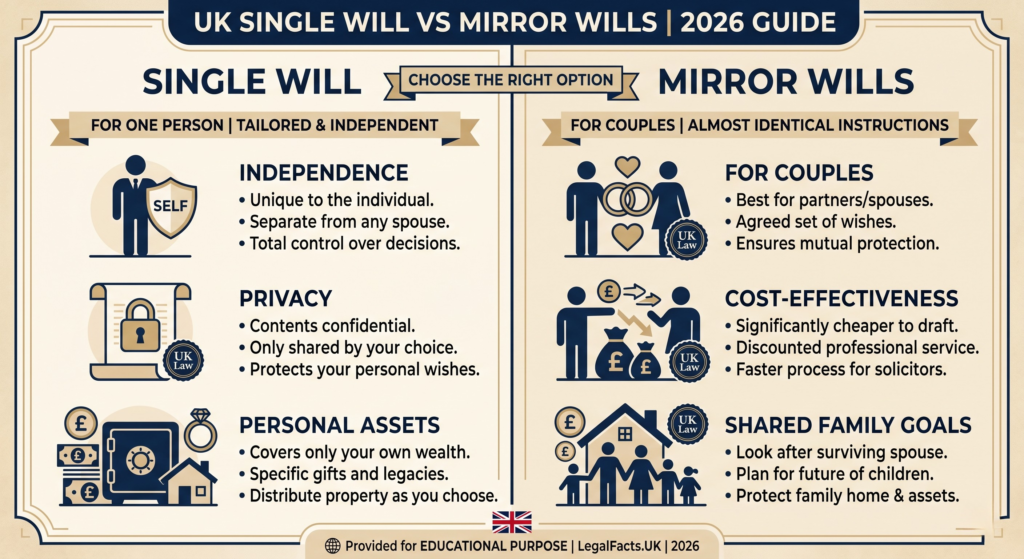

What is a Single Will?

A Single Will is an individual legal document created by one person. It is unique to you and only covers your own assets and wishes. Even if you are married, you are not legally required to have the same instructions as your spouse.

Independence and Privacy

The primary advantage of a Single Will is independence. You can decide exactly where your assets go without needing to consult anyone else. Furthermore, no one else has a right to see what’s in your Single Will while you are alive. This makes it the ideal choice for single people, divorced individuals, or even couples who have very different ideas about how their personal wealth should be distributed.

What is a Mirror Will?

Mirror Wills are two separate documents that are almost identical in their instructions. Usually, the setup is straightforward: Partner A leaves everything to Partner B, and vice-versa. If both pass away, the assets then go to a secondary set of beneficiaries, which are usually their children or a chosen charity.

The Advantages: Cost and Unity

From a practical standpoint, Mirror Wills are very popular because they are cost-effective. Most UK solicitors and online services offer a significant discount for Mirror Wills because the drafting process for the second Will is much faster. Beyond the cost, it provides a sense of unity, ensuring that the surviving spouse is looked after immediately and that both partners have agreed on the long-term future of their estate.

The Hidden Risk: The “Trust” Factor

The most important thing to remember about Mirror Wills is that they are not a legally binding contract between partners. This is a point that often surprises people.

If one partner passes away, the survivor inherits the assets and is then free to change their own Will at any time. This means they could potentially remarry and leave everything to a new spouse, or even disinherit children from the first marriage. This is often referred to as “Sideways Inheritance,” and it is a major reason why couples with children from previous relationships often avoid Mirror Wills in favor of more protected legal structures.

Common Myths About Mirror Wills

- Myth 1: People often assume Mirror Wills are legally binding for the survivor. In reality, they are independent documents, and the survivor has full legal autonomy to alter their terms post-death.

- Myth 2: Many believe they automatically protect assets from nursing home fees. However, they offer no specific protection against local authority care cost assessments.

- Myth 3: You must have the same executor. While common, you can appoint different executors in your respective documents based on who is best suited to handle specific asset types.

Which One Should You Choose?

There is no one-size-fits-all approach to estate planning. The decision often boils down to your specific family dynamics.

| Feature | Single Will | Mirror Will |

| Independence | Absolute | Limited by initial agreement |

| Flexibility | High | Medium |

| Best For | Blended families/Individuals | Stable, long-term partnerships |

| Cost | Standard | Generally lower (discounted) |

The Case for Mirror Wills

A Mirror Will is generally the best fit if you are in a long-term marriage or civil partnership where you share the same children and the same financial goals. If you trust your partner completely to uphold your shared wishes after you are gone—and your family situation is straightforward—the simplicity and lower cost of Mirror Wills make them a great choice.

The Case for Single Wills

On the other hand, a Single Will (or a Will containing a Trust) is much safer if you are part of a blended family. If you have children from a previous relationship, a Single Will allows you to ring-fence your specific assets. This ensures that your children are guaranteed their inheritance, regardless of whether your surviving partner remarries or changes their mind years down the line.

Frequently Asked Questions (FAQs)

1. Can one person change a Mirror Will without the other knowing?

While both partners are alive, if one person changes their Will, a solicitor is usually ethically bound to inform the other person if they are acting for both. However, after one partner dies, the survivor can change their Will in total secrecy without anyone’s permission.

2. Does remarrying cancel a Mirror Will?

Yes. In England and Wales, marriage usually revokes any existing Will automatically. This is a huge risk with Mirror Wills; if the surviving spouse remarries, the “Mirror” instructions are cancelled by law, and the new spouse may end up inheriting everything instead of the original children.

3. Are “Mutual Wills” the same as Mirror Wills?

No. Mutual Wills are a rare and very restrictive legal setup where both parties agree never to change the Will, even after one person dies. These are rarely recommended as they lack flexibility; Mirror Wills are the much more common standard.

4. Can we have Mirror Wills if we aren’t married?

Yes, cohabiting couples can (and should) have Mirror Wills. Since “common law” partners have no automatic inheritance rights in the UK, Mirror Wills are a vital way to ensure the surviving partner isn’t left financially vulnerable.

Commonly Asked Questions

- What is the downside of mirrored wills? The primary drawback is the lack of protection against future changes by the surviving partner, which can inadvertently disinherit intended beneficiaries.

- Do you need probate if you have a mirror will? Yes. Having a mirror will does not exempt your estate from the probate process upon your passing.

- What is the biggest mistake in drafting a will? Attempting a “DIY” approach without professional guidance often leads to ambiguous wording, which causes costly disputes during the probate process.

- What are the two main types of wills? While there are various forms, the primary categories for personal estate planning are Single Wills and Mirror Wills (with Mutual Wills being a rare, more rigid alternative).

Conclusion

There is no “one size fits all” in estate planning. Mirror Wills offer a beautiful symbol of shared goals and cost savings, but they require a high level of trust and a simple family structure. If your family tree has multiple branches, or you want a “guaranteed” protection for your children’s inheritance, a Single Will is often the more secure path to peace of mind.

Final Thoughts for UK Residents

Whether you lean toward the simplicity of a Mirror Will or the protective capacity of a Single Will, your primary objective should be clarity. In the UK, clear instructions prevent years of familial discord. Always review your documents every 3 to 5 years, or whenever a major life event occurs, such as a marriage, divorce, or the arrival of a new family member.

Important Disclaimer: Legalfacts.uk provides educational content. We are not solicitors. Choosing between Single and Mirror Wills can have long-term tax and inheritance implications. We recommend discussing your specific family dynamic with a qualified estate planner or solicitor.