How is the Family Home Divided in a UK Divorce?

For most couples in the UK, the family home represents much more than just a roof over their heads; it is often their most significant financial asset and the anchor of their family life. When a marriage breaks down, the question of “who gets the house?” frequently becomes the most emotionally taxing and complex part of the entire separation process.

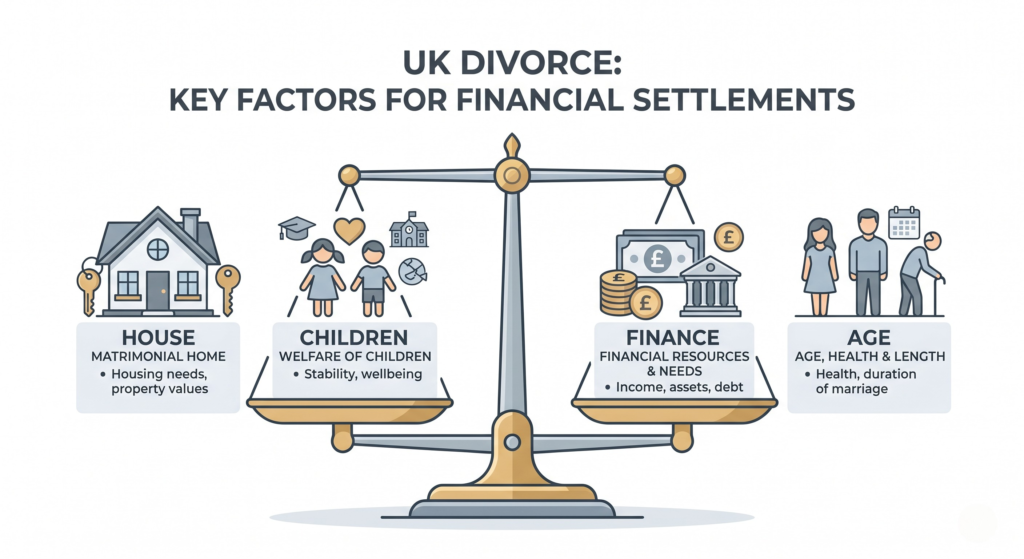

There is a widespread misconception that the law automatically mandates a 50/50 split, or that the person who paid the mortgage or the deposit is the sole “owner.” In the eyes of the UK family court, the reality is far more nuanced. The court’s guiding principle is not necessarily strict equality, but rather “fairness” and the fulfillment of the “needs” of both parties and any children involved.

In this guide, we will explore how the law determines the fate of the family home and the various pathways available to couples in 2026.

The Starting Point: Fairness, Not Just Equality

While the court often takes a 50/50 split as a baseline—particularly in long-term marriages—it frequently departs from this starting point. Under the Matrimonial Causes Act 1973, judges are required to weigh several specific factors to determine what constitutes a fair outcome.

The absolute priority is the welfare of any children under the age of 18. The court’s primary goal is to ensure they maintain a stable living environment. In many cases, this results in the primary caregiver remaining in the family home until the children reach a certain age or finish their education, prioritizing stability over an immediate financial liquidation of the asset.

Essential Factors Considered by the Court

When a judge reviews the situation, they look far beyond the title deeds. They must conduct a comprehensive assessment of the following:

- Financial Needs and Obligations: Where will each person live post-divorce? Can both parties realistically secure independent housing?

- Earning Capacity: The court evaluates the income and future earning potential of both individuals to see if one can maintain a mortgage while the other cannot.

- Marriage Duration: In short-term marriages, the court may be more inclined to restore the parties to their pre-marital financial positions. In long-term unions, assets are generally viewed as a shared “pot.”

- Age and Health: Does a partner have specific housing requirements due to age, retirement proximity, or disability?

- Non-Financial Contributions: The law recognizes that homemaking, childcare, and career sacrifices—which allowed one partner to focus on earning—are just as valuable as financial contributions.

Important Considerations: Non-Matrimonial Assets and Tax

In recent developments, the distinction between “matrimonial” and “non-matrimonial” assets has become increasingly vital. Assets brought into the marriage by one party (such as pre-marital property or certain inheritances) may be protected, provided they have been kept strictly separate. However, if these assets were “matrimonialised”—for example, by being used to purchase the family home or being mixed with joint finances—the court is likely to treat them as part of the shared pot.

Furthermore, it is critical to be mindful of tax implications. When transferring property between spouses during a divorce, there are specific “no gain/no loss” windows for Capital Gains Tax. Navigating these requires careful timing to avoid unnecessary financial penalties.

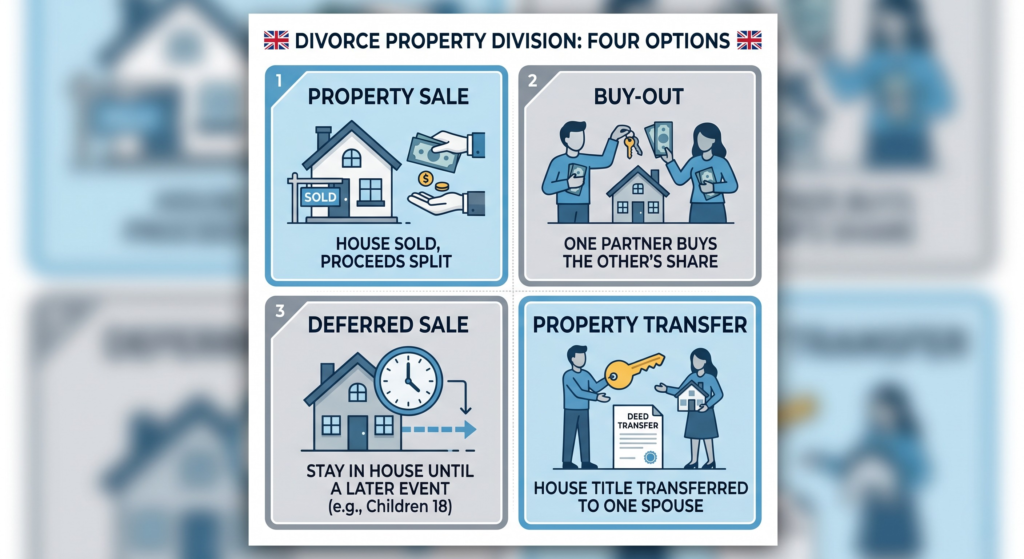

The Four Common Outcomes for the Family Home

Depending on your financial health and child-care arrangements, the court typically favors one of these four solutions:

- Selling the Home and Splitting Proceeds: This is the “clean break” option. The property is sold, the mortgage and associated costs are cleared, and the remaining equity is divided. This provides both parties with capital to start fresh.

- One Partner Buys the Other Out: If one person has the financial means—through savings, mortgage capacity, or offsetting other assets like pensions—they may “buy out” the other’s share. The departing spouse receives their equity share in cash, while the remaining spouse takes full responsibility for the property.

- The Mesher Order (Deferred Sale): This is common where children are involved. The house stays in joint names, and the primary caregiver remains in residence. The sale is “deferred” until a specified trigger event, such as the youngest child reaching 18 or completing university.

- Transfer of Property: A judge may order the title to be transferred entirely to one spouse. This is often part of a wider “offsetting” strategy, where one person keeps the house in exchange for the other retaining a larger share of the pension or other investments.

The Role of Mediation

Before heading to court, there is a strong emphasis on mediation. A Mediation Information and Assessment Meeting (MIAM) is often a necessary first step. Mediation allows couples to bypass the adversarial nature of court proceedings, keeping control over the outcome and significantly reducing the legal costs that can otherwise deplete your hard-earned equity.

Frequently Asked Questions (FAQs)

- Can my spouse force me to leave the house immediately?No. Unless a specific court order is in place or there is a genuine risk of domestic violence, both partners have a legal right to remain in the family home until a final financial settlement is reached.

- What if we can’t agree on the house value?You should appoint a RICS-qualified surveyor. If a disagreement persists, the court can appoint an independent expert whose valuation will be treated as the official figure.

- Does moving out mean I lose my rights to the home?Not at all. Moving out does not waive your legal claim to your share of the equity. However, always seek legal guidance before moving, as it can influence negotiations for arrangements like a Mesher Order.

- Who is responsible for the mortgage during the process?If the mortgage is joint, both parties are “jointly and severally liable.” This means the lender will hold both of you responsible if payments are missed. It is vital to reach a temporary agreement to ensure the mortgage is paid and your credit scores remain protected.

- What is a “Martin Order”?Similar to a Mesher Order, a Martin Order allows a spouse to reside in the property for life or until they remarry. This is often used for older couples or in cases where one partner has a significant disability that makes finding alternative housing difficult.

Conclusion

While the family home is often the most difficult subject to address, it is the most critical for your long-term security. The UK legal system offers flexibility to protect the interests of children and ensure fairness for both adults. Because every situation is unique, the most effective approach is to prioritize open negotiation or mediation. By reaching an agreement yourselves, you can minimize costs and preserve more of your family assets for the future.

Important Disclaimer: This is an informational article and does not constitute professional legal or financial advice. We strongly recommend consulting with a qualified solicitor and a tax professional to ensure your rights are fully protected during your separation.