How is Child Maintenance Calculated in the UK? (2026 Guide)

When parents decide to separate, the legal and moral responsibility to support their children financially remains, regardless of the custody arrangement or who the children live with. In the United Kingdom, this process is overseen by the Child Maintenance Service (CMS). For many, the calculation mechanism can feel like a complicated “black box”—you report your salary, and a figure emerges.

As we move through 2026, the system has become significantly more integrated with HMRC data. This digital connectivity makes it much harder to obscure income and ensures that the assessment process remains transparent and fair for both parties. In this guide, we will break down the exact formulas used by the CMS, how the system accounts for shared care, and how your specific family circumstances influence the final amount.

The Core Formula: Gross Weekly Income

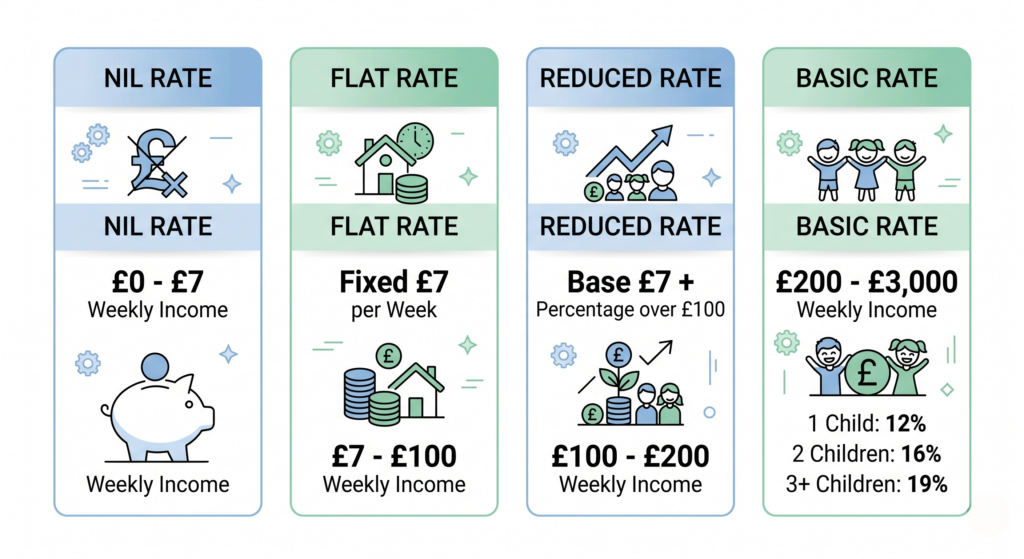

In 2026, child maintenance assessments are primarily based on the paying parent’s Gross Weekly Income. This represents your total income before tax and National Insurance deductions, but importantly, it is calculated after any contributions made to a private or workplace pension scheme have been removed.

The CMS follows a structured approach to determine your liability, primarily categorized by the “Rate” that fits your financial profile:

- Nil Rate (£0 – £7 weekly income): No maintenance payments are required.

- Flat Rate (£7 – £100 weekly income): A fixed payment of £7 per week is mandated, regardless of the number of children. This rate also applies if you are currently receiving certain state benefits.

- Reduced Rate (£100 – £200 weekly income): You pay a base of £7, plus a small percentage of your income that exceeds the £100 threshold.

- Basic Rate (£200 – £3,000 weekly income): This covers the vast majority of cases. The rates are calculated as follows:

- 12% for one child.

- 16% for two children.

- 19% for three or more children.

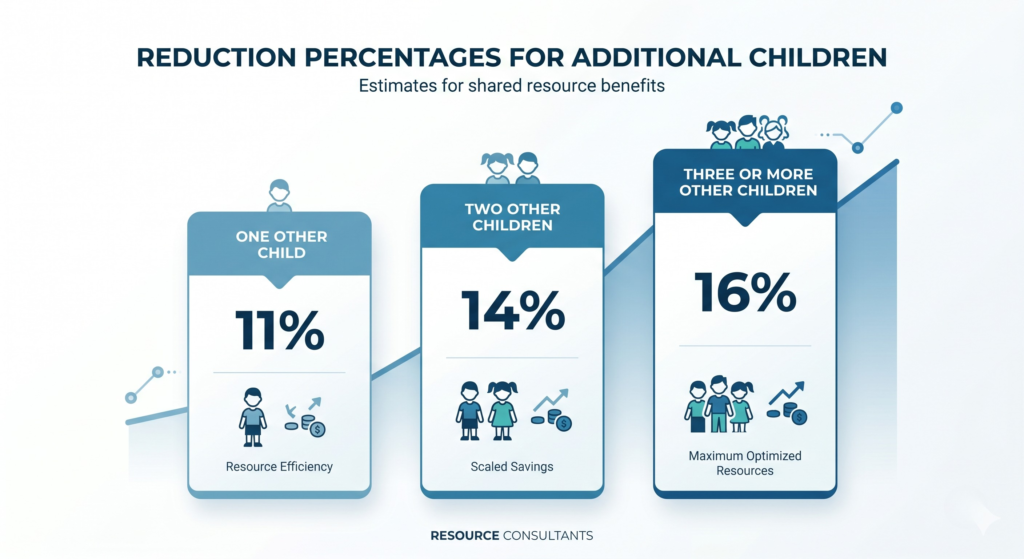

Reductions for “Other Children”

The CMS acknowledges that a paying parent may have additional financial obligations to other children living within their current household, such as those from a new marriage or partnership. To maintain fairness, the “exigible income” (the income used for the calculation) is reduced before the maintenance percentage is applied:

- 11% reduction for one other child.

- 14% reduction for two other children.

- 16% reduction for three or more other children.

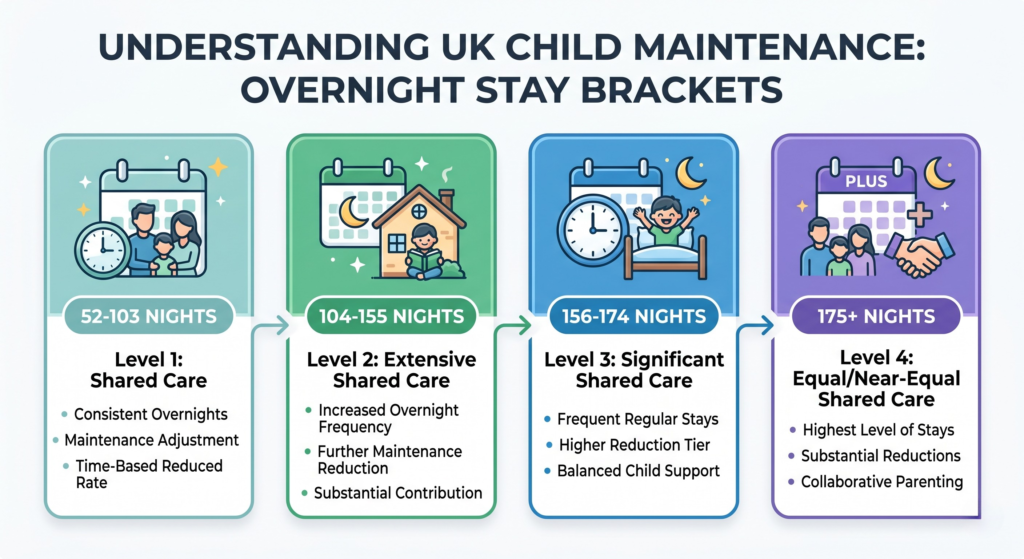

How Shared Care Impacts the Total

The amount of time a child spends overnight with the paying parent directly influences the maintenance liability. This is measured by the number of “overnight stays” per year. The logic is that the parent providing the care is already covering daily costs like food and utilities during those periods.

- 52 to 103 nights: A 1/7th reduction is applied.

- 104 to 155 nights: A 2/7th reduction is applied.

- 156 to 174 nights: A 3/7th reduction is applied.

- 175 nights or more: If care is shared equally, the maintenance is reduced by 50%, plus an additional £7 per week per child.

High Earners and the £3,000 Cap

The CMS authority is limited to income up to £3,000 per week, or £156,000 per year. For parents earning above this ceiling, the receiving parent has the option to apply to the court for a “Top-Up Order.” Throughout 2026, courts have shown an increased focus on transparency regarding these orders, aiming to ensure that children of high-earning parents continue to enjoy a standard of living that reflects the parent’s overall wealth.

Additional Financial Factors to Consider

To ensure your financial planning is accurate, it is helpful to keep these additional elements in mind:

- Non-Resident Parent’s Expenses: While the core calculation focuses on income, the CMS does allow for “variations” in specific circumstances. This includes costs like paying for a child’s disability-related needs or significant travel expenses incurred to maintain contact with the child.

- Pension Contributions: Because pension payments are deducted before the calculation, maximizing your pension contributions can legally lower your “Gross Weekly Income,” thereby impacting your total maintenance liability.

- Income Fluctuations: If you are a freelancer or have irregular income, the CMS generally averages your earnings over the most recent tax year. If you expect a significant long-term dip in income, it is essential to communicate this immediately rather than waiting for the annual review.

- Voluntary Agreements: Many parents choose to reach a private agreement rather than involving the CMS. While these agreements are not legally enforceable in the same way, they can offer more flexibility, provided both parents are in complete agreement and prioritize the child’s needs.

Frequently Asked Questions (FAQs)

1. Does the CMS take my partner’s income into account? No. The calculation is based solely on the income of the paying parent. The financial situation of a new partner or an ex-partner’s new spouse is irrelevant to the CMS assessment.

2. What if the paying parent is self-employed? The CMS accesses data directly from HMRC to determine “Total Self-Employed Profit” from the latest tax return. If there are concerns that income is being retained within a limited company to avoid payments, a “Variation” can be requested to investigate dividends and company assets.

3. Is there a fee for using the CMS? If you choose the “Direct Pay” service, where the CMS performs the calculation but parents manage the transfer themselves, there are no service fees. However, if the “Collect & Pay” service is used, a 20% surcharge is added for the payer, and a 4% fee is deducted from the receiver.

4. What happens if I lose my job? You are required to inform the CMS immediately. If your income decreases by 25% or more, they will trigger a recalculation. In 2026, the digital self-service portal allows for the uploading of redundancy documentation for a faster adjustment.

5. Can maintenance be paid until the child is 21? Standard payments usually end when the child reaches 16, or 20 if they are in approved full-time “non-advanced” education, such as A-levels or equivalent. If a child enters University, a separate court order is often required for support regarding tertiary education.

Conclusion

The UK child maintenance system is built as a standardized mathematical framework, aimed at removing the conflict often associated with determining “fair” support. While it may seem rigid, the objective is to provide consistency for the child. By fully grasping the income bands, the impact of shared care, and how your household size influences the numbers, you can ensure your assessment is correct. Ultimately, child maintenance is not a fee for contact; it is a vital, fundamental obligation to ensure a child’s needs are met by both parents.

Important Disclaimer: This content is for informational purposes only and does not constitute legal or financial advice. We are not solicitors. As regulations regarding child maintenance and HMRC data integration can evolve, we highly recommend verifying your specific situation using official government resources or consulting with a qualified legal professional.