When a marriage breaks down, the focus often shifts to the immediate challenges: ‘Who gets the house?’ or ‘How will we split the savings?’ Amidst the emotional toll of a separation, one of the most significant assets is frequently overlooked: divorce and pensions. In many UK households, the combined value of private and workplace pension schemes can actually exceed the value of the family home, making it a critical part of your financial settlement.

Ignoring this asset is a mistake that can lead to severe financial hardship in your later years. In the United Kingdom, the law views pensions as a joint asset. This means that even if the pension is in your spouse’s name, you may be entitled to a portion of it. This guide explores the complexities of pension splitting in the UK, ensuring you understand your rights to secure your financial future.

1. The Legal Foundation: Why Pensions Matter

In the UK, the “matrimonial pot” is a legal concept that encompasses all assets acquired during the marriage. Courts have a clear mandate: to ensure a fair outcome for both parties. Because pensions are designed to provide long-term income, they are often the most complex asset to divide.

If one partner sacrificed their career progression to care for children or manage the household, their retirement contributions may have suffered. The law recognizes this sacrifice. When a judge looks at a settlement, they don’t just look at who “earned” the money; they look at the contribution made by both parties to the marriage.

2. What Exactly Is Included?

Many couples mistakenly believe that only current workplace pensions are up for debate. The reality is much broader. A comprehensive settlement should involve:

- Workplace Pensions: This includes Defined Contribution schemes (where the value depends on investments) and Defined Benefit schemes (where you are promised a specific income based on salary and service).

- Private/Personal Pensions: Such as SIPPs or stakeholder pensions managed by independent providers.

- Additional State Pensions: While the basic State Pension is not divisible, the “Additional” portions (like SERPS or S2P) that accrued during your marriage can be factored into a settlement.

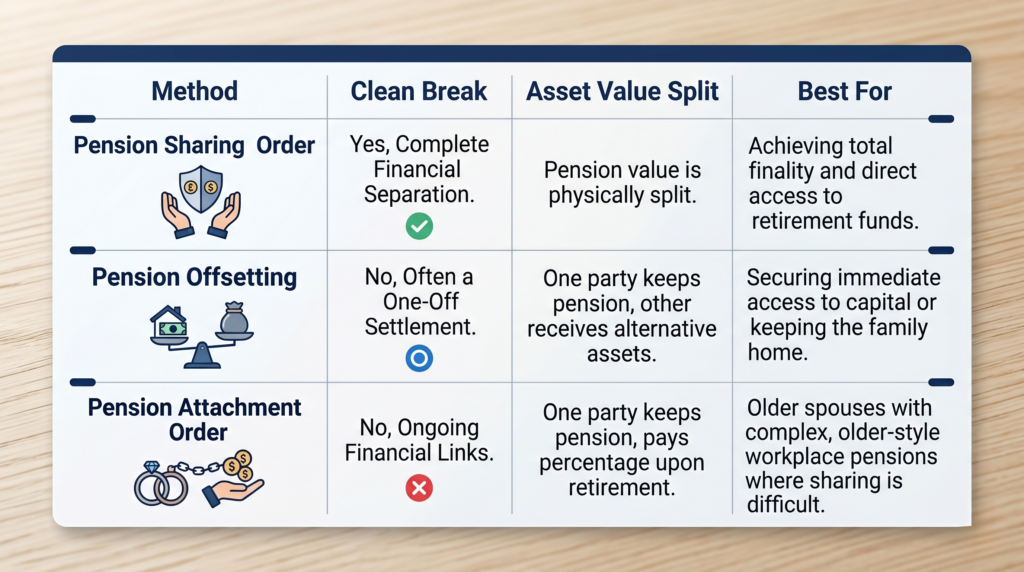

3. The Three Methods of Pension Division

Once the valuation is complete, you and your solicitor must decide how to handle the split. In the UK, there are three primary legal avenues.

A. Pension Sharing Order (The Clean Break)

This is widely considered the most effective method by legal experts. Under a Pension Sharing Order (PSO), a percentage of one spouse’s pension is legally carved out and transferred into a brand-new pension pot for the other spouse.

- The Advantage: It provides a “clean break.” You no longer need to rely on your ex-spouse’s financial health or wait for them to retire to access your portion. Once transferred, the money is fully yours to control, invest, and eventually withdraw.

B. Pension Offsetting

If a couple has significant non-pension assets—such as the family home—they may choose to offset. Instead of splitting the pension, one person might keep their full pension, while the other receives a larger share of the home’s equity or cash savings.

- The Strategy: This is common when couples want to minimize legal costs or avoid the complexities of splitting pension schemes. However, it requires a precise valuation of both the pension and the property to ensure the deal remains equitable.

C. Pension Attachment Order (Earmarking)

This is a more dated approach. The court orders that when one spouse eventually begins drawing their pension, a specific percentage of that income is diverted to the ex-spouse.

- The Downside: This is not a clean break. You remain linked to your ex-spouse financially. If they choose to defer their retirement, you wait. If they pass away, you may face significant uncertainty regarding your future income.

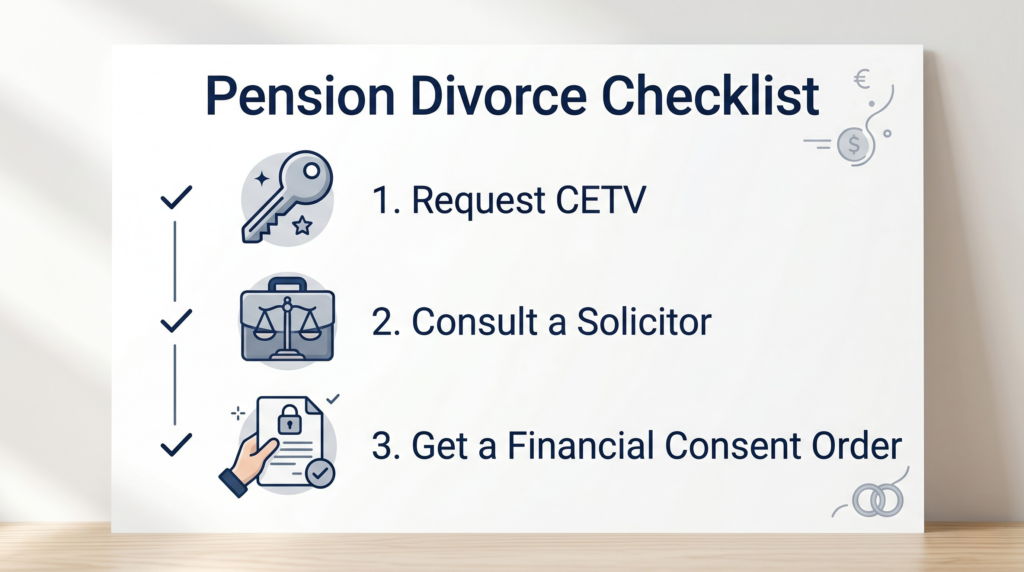

4. The Crucial Step: Valuation and the CETV

Before any agreement is reached, you must obtain a Cash Equivalent Transfer Value (CETV) from the pension provider.

Important Warning: The CETV is a snapshot, but it is not always the full story. For public sector pensions (like those for teachers, the NHS, or the police), the CETV may drastically underestimate the true value of the “guaranteed” income that the pension will pay out over a lifetime. In such scenarios, hiring a specialist pension actuary is not just an expense—it is an investment in your own future security.

5. Frequently Asked Questions (Expert Insights)

Will my ex-spouse be able to claim my pension years later?

Without a Financial Consent Order that includes a “clean break” clause, your finances are never fully severed. An ex-spouse can technically return to court years later to make a claim on your retirement assets. Always ensure your divorce settlement is legally formalised.

Is the split always 50/50?

The court’s priority is “needs,” not necessarily an equal split. If one partner has a much higher earning potential or is significantly younger, the court might lean towards a 60/40 or 70/30 split to ensure both individuals can maintain a reasonable standard of living after retirement.

Does remarrying impact my pension share?

If you have secured a Pension Sharing Order, the money is yours to keep, regardless of whether you remarry. However, if you rely on an Attachment Order, those payments are often conditional and may cease the moment you enter into a new marriage.

What is the biggest mistake people make?

The biggest mistake is focusing exclusively on the present while ignoring the future. A divorce is an emotional time, but don’t let that cloud your judgment. Signing a settlement without getting the pension values checked by a professional is a decision you may regret when you hit retirement age.

Conclusion

Navigating the division of pensions during a divorce is rarely straightforward, but it is a fundamental step toward securing your future. By understanding the differences between sharing, offsetting, and earmarking, you move from a position of vulnerability to one of empowerment.

Whether you choose to keep the family home or prioritize your pension, ensure that every decision is backed by accurate data and professional guidance. Your future self will thank you for taking the time to get this right today.

Disclaimer: This article is provided for informational purposes and does not constitute professional legal or financial advice. Pension legislation is highly technical and subject to change. We strongly recommend consulting with a qualified UK solicitor and an independent financial adviser (IFA) to discuss your unique circumstances.

James Whitfield is a senior legal researcher with over a decade of experience in UK family law and civil rights. He founded LegalFacts.uk to make complex legal information simple and accessible for everyday people across the United Kingdom.