Inheritance Tax UK 2026 rules caught my family completely off guard. My dad passed away last year, and I genuinely thought Inheritance Tax was something that only applied to people with castles and offshore accounts. Turns out, his three-bedroom semi in Surrey — bought for £40,000 back in the 80s — was suddenly “worth” enough on paper to drag us into a conversation with HMRC that none of us were prepared for.

If you’re reading this because you just got a letter, or because you’re trying to get ahead of the problem before it becomes a problem, I get it. I spent weeks on the phone with solicitors, googling things at 11pm, and filling out IHT400 forms with a cup of tea going cold beside me. So here’s everything I picked up — the practical stuff, not just the textbook version.

Why Inheritance Tax UK 2026 Catches So Many Families Off Guard

Here’s the thing nobody really tells you: the tax-free allowance hasn’t moved in years. The standard Nil-Rate Band has sat at £325,000 since 2009, and it’s now frozen all the way until 2030 (some recent Budget announcements have even pushed talk of an extension further out). Meanwhile, house prices — especially anywhere near a city — have gone in the opposite direction entirely.

That’s the trap. You’re not “rich” in any meaningful sense. You just own a house in the wrong postcode at the wrong time, and suddenly your estate is brushing up against a threshold that was set when fuel was under a pound a litre.

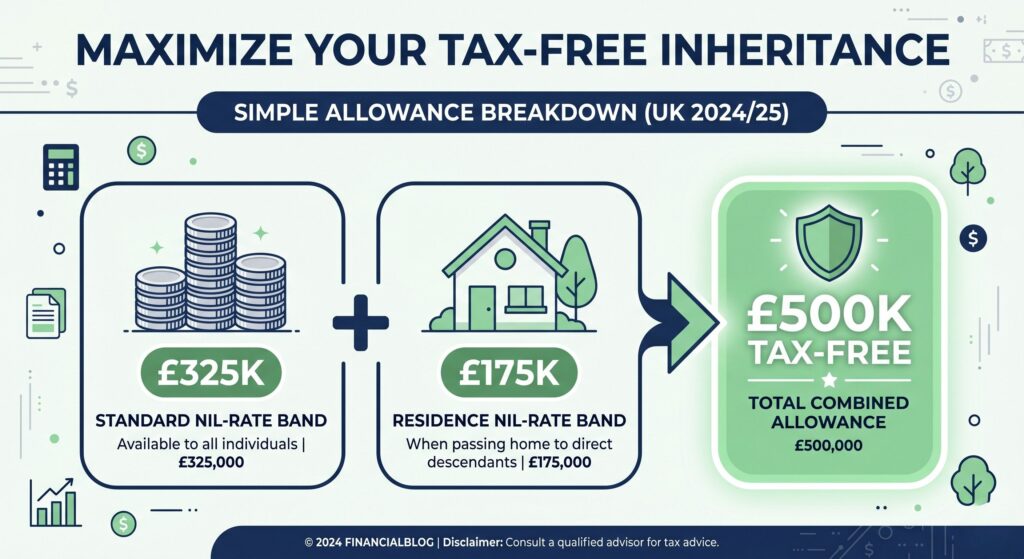

Inheritance Tax UK 2026 Allowances: What You Can Actually Pass On Tax-Free

This is the part I wish someone had explained to me in plain English instead of legal jargon.

1. The Standard Nil-Rate Band — £325,000

Every person gets this automatically. If your whole estate — house, savings, car, that weird coin collection in the attic — adds up to less than £325,000, there’s nothing to pay.

2. The Residence Nil-Rate Band — £175,000

This one only kicks in if you’re leaving your main home to children, grandchildren, step-children, or similar “direct descendants.” It does NOT apply if you’re leaving the house to a niece, a friend, or a charity (though charities have their own separate exemption, more on that below).

Add the two together and a single person can shelter up to £500,000. Married couples and civil partners can combine both of their allowances, which means a surviving spouse can potentially pass on up to £1 million completely tax-free. This is the number that saved my family a huge headache — my mum inherited everything from my dad tax-free under spousal exemption, and his unused allowance simply transferred to her.

One thing that trips people up: if your total estate creeps past £2 million, the Residence Nil-Rate Band starts shrinking — you lose £1 of it for every £2 over that line, and it disappears completely once you’re past roughly £2.35 million (or around £2.7 million for a couple). If you’re anywhere near that territory, this isn’t a DIY situation — get a proper adviser involved.

How the 40% Tax Actually Works

Everything above your combined allowance gets taxed at a flat 40%. That’s it — no sliding scale, no mercy for “but the house was a gift from my grandmother.”

A simple example: say a single person dies with an estate worth £600,000, and they qualify for the full £500,000 allowance. The taxable slice is £100,000, and 40% of that is a £40,000 bill. That’s real money the estate has to find, often before probate can even finish — which is its own nightmare if most of the estate is tied up in a house that hasn’t sold yet.

A trick I only found out about afterwards: if you leave at least 10% of your net estate to a registered charity, the rate on everything else drops from 40% down to 36%. My dad’s will had a small donation to a local charity built in, and it genuinely made a difference to the final bill. If you’re writing or updating a will, this is worth discussing with whoever’s drafting it.

The Big 2026 Shake-Up: Farms and Family Businesses

This is where things have properly changed this year, and if you or your family run a business or a farm, pay attention here because the rules used to be far more generous.

Up until recently, Agricultural Property Relief (APR) and Business Property Relief (BPR) gave 100% relief with no real cap — meaning a family farm or business could pass down completely tax-free regardless of value. As of April 2026, that’s no longer the case.

There’s now a combined cap of £1 million per person on qualifying agricultural and business assets that get full 100% relief. Anything above that £1 million gets only 50% relief, which works out as an effective 20% tax rate on the excess (rather than the usual 40%). This allowance is also transferable between spouses now, following some late amendments to the original proposal — so a married couple running a business together effectively get £2 million of combined protection.

If your family has farmland or a business that’s been quietly appreciating for decades, this is genuinely one of the biggest IHT changes in years and it’s worth getting a valuation and a proper conversation with an accountant sooner rather than later — there’s even an option now to pay any resulting tax over 10 interest-free annual instalments, which softens the blow if you don’t want to sell land or shares to cover it.

Gifting: The Strategy That Actually Worked for Us

This is the bit that made the biggest practical difference for my own planning once I’d been through the process with my dad’s estate.

- The 7-Year Rule — Give away a large gift and survive 7 years, and it falls completely outside your estate for tax purposes. Die within those 7 years and there’s a sliding scale (taper relief) that reduces the tax owed the longer you survived.

- Annual Exemption — You can give away £3,000 every single year, no questions asked, no waiting period.

- Small Gifts Allowance — Up to £250 per person, to as many different people as you like, every year.

- Wedding Gifts — Up to £5,000 to your own child, £2,500 to a grandchild, or £1,000 to anyone else getting married.

My honest advice: start the £3,000 annual gifting early and keep records. We found a shoebox of old bank statements that helped prove some of my dad’s gifts were within the rules, and it saved a back-and-forth with HMRC that could’ve dragged on for months.

Mistakes I Made (So You Don’t Have To)

- I assumed the house value HMRC wanted was the same as the “Zoopla estimate.” It isn’t. You need a proper RICS valuation for probate purposes, and undervaluing the property can cause real problems later if HMRC disagrees.

- I didn’t realise IHT has to be paid within 6 months of death — not after probate is granted, not “whenever the house sells.” If it’s late, HMRC starts charging interest, and that clock doesn’t wait for your paperwork to catch up.

- I thought pensions were automatically outside the estate. For 2026 most pensions are still largely protected, but that’s changing — from April 2027, most unused pension pots and death benefits are due to be brought into the IHT calculation for the first time. If a chunk of your retirement planning sits in a pension specifically because you thought it skipped IHT entirely, it’s worth checking with your provider now rather than waiting.

- I left it too late to talk to a solicitor. I tried to handle the first IHT400 form myself. It’s not impossible, but it’s genuinely time-consuming, and one mistake on valuations or reliefs claimed can delay probate by weeks.

Frequently Asked Questions About Inheritance Tax UK 2026

How much is Inheritance Tax in the UK in 2026?

The rate itself is a flat 40% on the portion of an estate above the available tax-free allowance. For most people, that allowance is £325,000 (the standard Nil-Rate Band), rising to £500,000 if you’re leaving a home to direct descendants, thanks to the additional £175,000 Residence Nil-Rate Band.

Is UK Inheritance Tax going to change?

The core thresholds (£325,000 and £175,000) are frozen and aren’t expected to move before 2030, with some recent Budget commentary suggesting the freeze could be extended even further. The bigger changes are happening around the edges — agricultural and business property relief tightened from April 2026, and pensions are due to be pulled into the IHT net from April 2027.

What are the tax changes for 2026 in the UK?

The headline change is the new £1 million combined cap on 100% Agricultural Property Relief and Business Property Relief, with only 50% relief above that. There’s also a new option to pay IHT on qualifying business/agricultural assets over 10 interest-free annual instalments, which is a genuinely useful cash-flow change for families who don’t want to sell land or shares to cover a bill.

How much can you inherit in the UK before paying Inheritance Tax?

As a recipient, you generally don’t pay IHT directly out of your own pocket — it’s deducted from the estate before you receive anything. The estate itself can pass on up to £325,000 tax-free (or £500,000 with the residence allowance, £1 million for a married couple using both sets of allowances) before the 40% rate applies to the rest.

Final Thoughts on Inheritance Tax UK 2026

Going through this with my own family taught me that Inheritance Tax isn’t really about being wealthy — it’s about being unprepared. The thresholds haven’t moved, property prices have, and the rules around farms, businesses, and now pensions are shifting under everyone’s feet. None of it is unmanageable if you know roughly where you stand and start the conversation early, whether that’s gifting sensibly, updating a will, or just getting a proper valuation done before you need one.

If your estate is anywhere near these numbers, don’t wait for a letter from HMRC to figure it out — have the conversation with a solicitor or tax adviser now. It’s a much easier chat to have when nobody’s grieving and there’s no clock running.

This article is for general information based on personal experience and publicly available rules current as of mid-2026. It isn’t financial or legal advice — Inheritance Tax rules are genuinely complicated and estate-specific, so please speak to a qualified solicitor or tax adviser about your own situation.

David Hargreaves is a legal content writer specialising in wills, inheritance, and cohabitation rights. He is passionate about helping UK residents understand what happens to their assets and loved ones, and writes in-depth guides to make the law easy to understand for everyone.